All goods or services within an economy begin with a query: how is it produced? The answer lies in the factors of production, the key resources needed to create goods and services. The elements of production consist of land, labor, capital, and entrepreneurship, while including contemporary elements of technology and human capital. Students, entrepreneurs, and policymakers will benefit from understanding these production inputs because they will help them make better choices.

What Are Factors of Production?

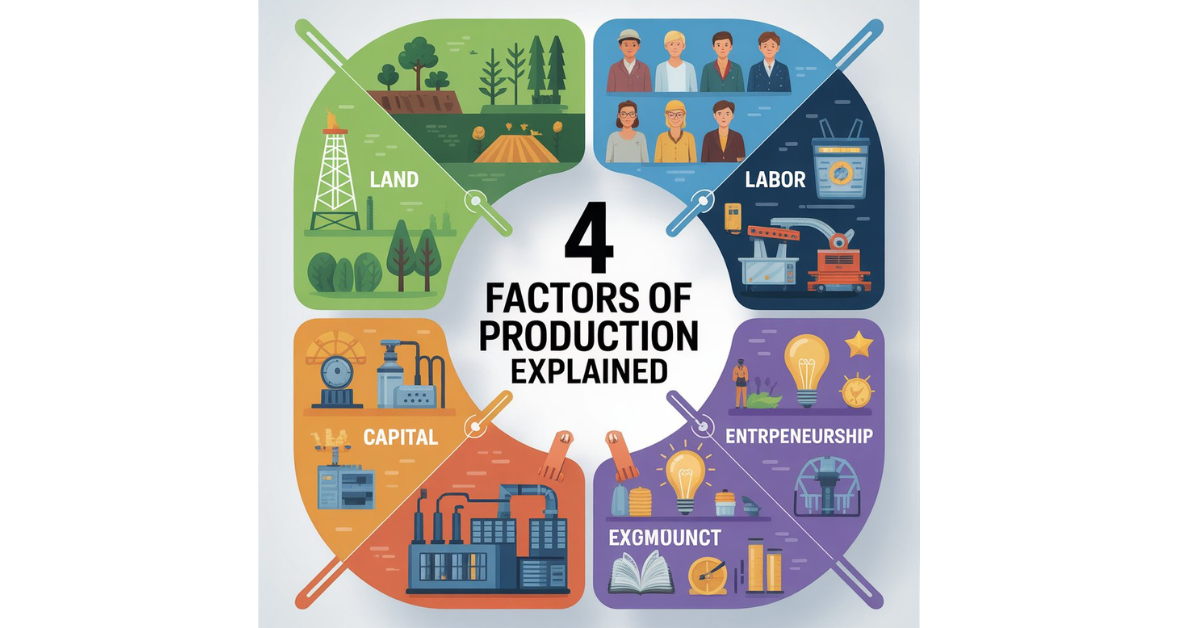

The Factors of Production are the resources used to process goods and services. They are normally grouped into four major categories by economists: land, labor, capital, and entrepreneurship. These inputs are incorporated in the production process and converted into raw materials to be used into output.

To put it in plain language, no economy will run without inputs of production. All products, including food and clothing, software, and medical services, need a combination of natural resources, workforce, equipment, and judgment. This is the basis of the economics theory and how companies distribute the limited resources in the most effective and efficient manner.

The Four Main Production Factors Explained

Land

In economics, land includes everything that is used in production, not necessarily physical land. The resource base includes water resources, forest areas, mineral deposits, oil reserves, and climate conditions. Land may be renewable through agricultural soil or non-renewable through coal and natural gas.

Farming operates with essential requirements of fertile land and water resources, while mining requires access to underground mineral deposits.

Labor

Labor is human input, physical and mental, that is applied in production. It comprises skilled and unskilled employees, professionals, and technical experts. In contemporary economics, the quality of work is more than the quantity.

It is here that human capital in economics comes in. Training, education, and experience enhance the productivity of workers and heighten the level of output. An example would be a skilled software developer would add more value than unskilled labor in the technology sector despite having fewer working hours.

Capital

Capital consists of man-made techniques and machines on which goods and services are produced. Under capital, there are machinery, factories, tools, computers, and infrastructure. It should be pointed out that money is not capital, it is just useful in obtaining capital goods.

A capital example is a machine used in a factory to produce shoes, since as an example, the machine itself is capital, whereas the cash is not capital. The capital investment improves production efficiency, and it enables businesses to scale operations as time passes.

Entrepreneurship

Entrepreneurship refers to the capability to organize, manage, and risk by bringing together land, labor, and capital. Entrepreneurs are the people behind the making of important business decisions, innovation, and responding to demand in the market.

Other inputs of production will not be fully utilized without entrepreneurship. An entrepreneur who is starting a new product, raising funds, and recruiting employees illustrates the role of entrepreneurship in economic action and the generation of value in competitive markets.

Rewards of Production Factors

Production of each factor generates a certain kind of income, generally referred to as factor payments. Such incentives encourage people and companies to provide resources in an efficient manner.

- Land earns rent

- Labor earns wages

- Capital earns interest

- Entrepreneurship is profitable.

These payments assist in the allocation of income in the economy. As an example, increased wages invite skilled labor, whereas profits encourage innovation and risk-taking. The knowledge of factor rewards also gives an explanation to distribution of income in an economy.

Modern View of these Factors

Classical economics considered four variables, whereas contemporary economists identify new variables that determine productivity. Technology as a production factor is significant in the contemporary world as it enhances efficiency without the need to increase physical factors.

The total factor productivity can increase in the form of knowledge, innovation, and digital infrastructure, which enables firms to generate more using the same resources. As an example, the automation software will maximize output and minimize the cost of labor. This contemporary school of thought assists in the growth of the economy in developed and digitalized economies.

Production Factor in Real-World Industries

The application of Production Factors varies across industries. In the agricultural industry, land and labor prevail, and manufacturing is capital-intensive and has a high level of skilled labor. The service industry is more reliant on human capital and entrepreneurship.

An illustrative example is the case of a tech company that needs very little land yet vast talent, capital and leadership. These disparities demonstrate why inputs to production should be matched to industry requirements in order to produce efficiency and profitability.

Why Production Factors Are Important

These factors determine an economy’s productive capacity. The effective utilization of resources results in increased production, reduced expenditure, and the sustainable growth of the economy. Nations that have a good workforce, capital investments, as well as innovation perform better than those that lack resources.

To businesses, it would enhance planning, budgeting, and scalability of production input. The government uses this information to develop educational policies which develop educational systems, build physical facilities, and encourage businesses to use modern technological solutions for their sustainable economic growth.

Frequently Asked Questions

What is the reason why money is not a production factor?

Money simply eases transactions. It is not the direct manufacturer of goods or services as machinery or labor is.

Is technology a production factor?

Contemporary economics usually perceives technology as an efficiency factor that increases total factor productivity.

How do factors of production affect GDP?

Increased production inputs of lower quality lead to higher output, directly lifting GDP.

Conclusion

The factors of production form the backbone of every economy by explaining how goods and services are created. Since natural resources and skilled labor contribute to the production process, as well as capital investment and entrepreneurship, the role of each of them is different. The modern economy is further fueled and increased with technology and knowledge. By having a problem of how inputs of production interact, individuals and businesses can make better economic choices, and their structures can adjust with the changed needs of the market.